Posted on: Wednesday, March 13, 2024

Signs of green shoots are appearing in the property market. More buyers are returning to the market, supported by falling mortgage rates, wage growth outstripping inflation, and a strong labour market.

With the Bank of England holding the interest rate at 5.25%, the consensus is that we are at the top of the rate rise cycle. Interest rate expectations in the monthly consensus forecasts have been improving over recent months as the economic outlook brightens (HM Treasury Average of Independent Forecasts). Rates are predicted to start falling in the second half of the year, reaching 4.4% by the end of 2024. With inflation under control and forecast to fall to 2.2% by the end of the year (HM Treasury Average of Independent Forecasts), confidence in the housing market is improving.

With the Bank of England holding the interest rate at 5.25%, the consensus is that we are at the top of the rate rise cycle. Interest rate expectations in the monthly consensus forecasts have been improving over recent months as the economic outlook brightens (HM Treasury Average of Independent Forecasts). Rates are predicted to start falling in the second half of the year, reaching 4.4% by the end of 2024. With inflation under control and forecast to fall to 2.2% by the end of the year (HM Treasury Average of Independent Forecasts), confidence in the housing market is improving.

In the year to February, average rents across the UK rose by 7.4% to £1,262. Average rents increased by 0.2% January to February, with all regions seeing a monthly rise except for the South East, Yorkshire and the Humber, Wales, Northern Ireland and London (HomeLet). Rents are still forecast to rise in 2024, albeit at a slightly slower pace. A net balance of +41% of agents envisage rents rising over the next three months, as demand continues to outweigh supply (RICS). However, many landlords are keen to keep existing renters: 75% would maintain a rent level if they were happy with the existing renter, rather than take a new renter who would pay more (Dataloft, Property Academy Landlord Survey 2023).

The Chancellor has also abolished the furnished holiday lettings tax regime, which should help to level up the buy-to-let sector and unlock more full-time tenancy stock in major cities, tourist hotspots and coastal communities.

Early signs for the market in 2024 are increasingly positive, with metrics for buyer demand, sales and new instructions all turning positive (RICS). Choice for buyers is on the rise, with available homes for sale 20% higher than a year ago (Zoopla). Improved market conditions are boosting the chances of a sale, although sellers must continue to present their property well and at a reasonable price if they are serious about moving in 2024. Half of agents say offers are currently being accepted up to 5% below initial asking price; however, 15% report this level or higher (Dataloft Inform Poll of Subscribers).

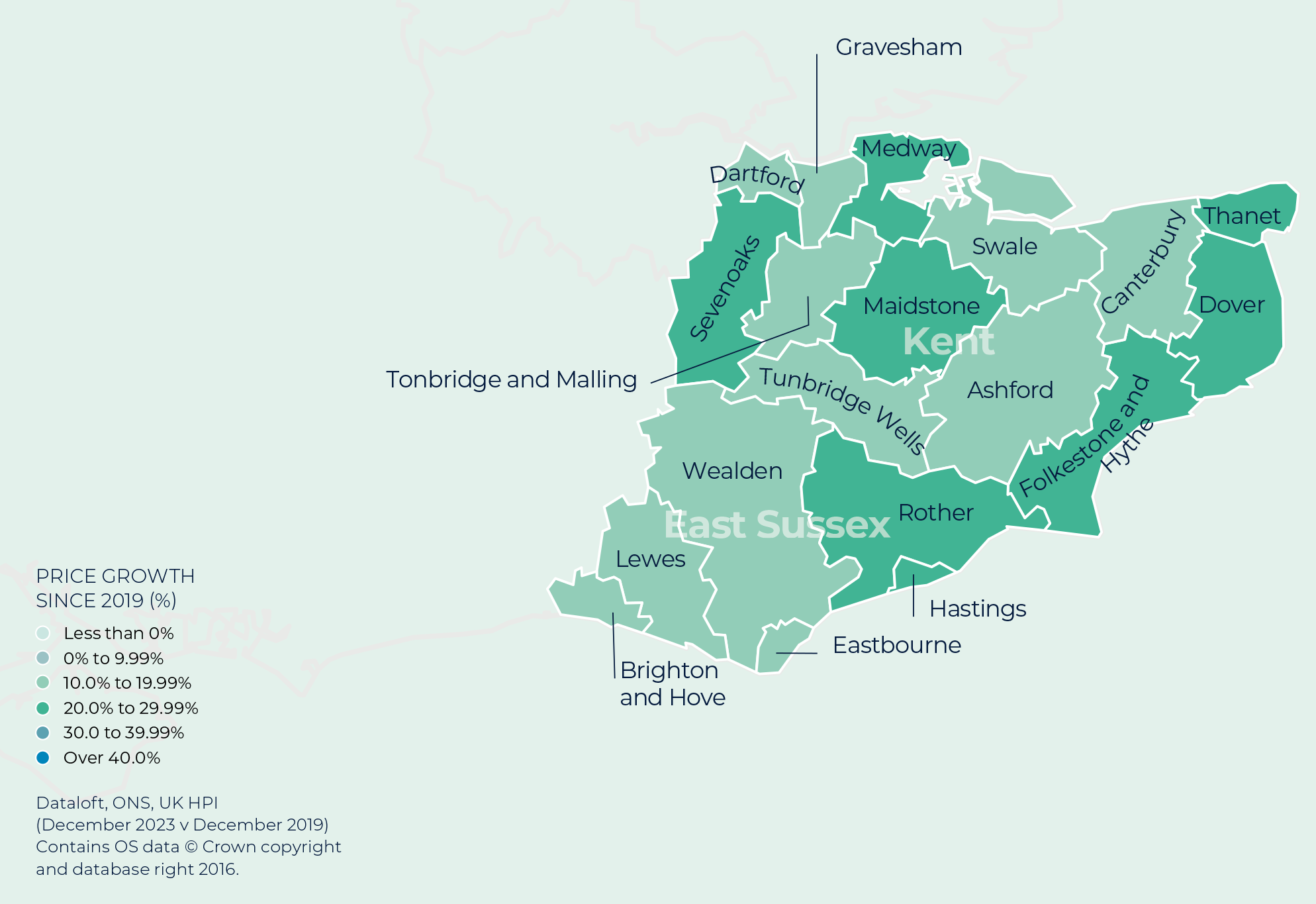

Average property values in the South East are 17% above 2019 levels, equivalent to a rise of £55,884, above 2019 levels (UK HPI December 2023). Price growth since before the pandemic is strongest in Medway and Rother.

Sell your property with your local expert this spring. Contact your local Guild Member today.

We are required by law to conduct anti-money laundering checks on all those selling or buying a property. Whilst we retain responsibility for ensuring checks and any ongoing monitoring are carried out correctly, the initial checks are carried out on our behalf by Lifetime Legal who will contact you once you have agreed to instruct us in your sale or had an offer accepted on a property you wish to buy. The cost of these checks is £60 (incl. VAT), which covers the cost of obtaining relevant data and any manual checks and monitoring which might be required. This fee will need to be paid by you in advance of us publishing your property (in the case of a vendor) or issuing a memorandum of sale (in the case of a buyer), directly to Lifetime Legal, and is non-refundable. We will receive some of the fee taken by Lifetime Legal to compensate for its role in the provision of these checks.